The agriculture industry has automated many parts of their processes; however, the forestry industry still depends on manual labor to plant seeds in the ground in harsh and uneven terrain – drones could be the solution to replace these tedious and dangerous tasks (see article).

§179: Accelerating Cost Recovery for Horse Businesses

Section 179 is a very business friendly tax provision meant to give small to medium-sized businesses the tax incentive to purchase qualified property. When combined with §168 MACRS deduction, and §168(k) Bonus Depreciation (to be discussed in a later post), those in the horse business can usually recover a significant amount of their depreciable costs immediately.

Although a generous tax provision, §179 is subject to three limitations:

- Type of property – qualified property must generally be new and used tangible property, but also may include computer software and real property, as specified in §1245(a)(3). Horses qualify.

- Dollar limitation – the maximum expense allowable starting in tax year 2016 is $500,000, and is reduced dollar-for-dollar over $2,000,000 of the aggregate costs of those qualified properties placed in service in the same taxable year. Both amounts will be indexed to inflation.

- Income limitation – bars a taxpayer from expensing an amount greater than their taxable income (including wages and salaries) from the active conduct of all their trades or businesses. Section 179 may not by itself create or increase a loss, and any excess not used in that taxable because of the income limitation may be carried over to the next taxable year.

Section 179 is also useful because it provides taxpayers with significant planning opportunities:

- The taxpayer can allocate their deduction amounts among their qualified property, meaning that they may want to consider applying their section §179 amounts first to those qualified properties that depreciate slower than others.

- Applying §179 to an asset may impact whether the half-year or mid-quarter convention applies to those assets placed in service in a taxable year.

Note that §179 property is subject to the recapture rules so that any prior §179 expense may have to be recaptured as ordinary income if the asset is later sold.

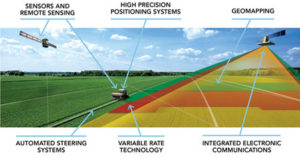

From Drone To Tractor – How Using A Precision Farming UAV Can Improve Crop Management

Precision farming (“PF”) is a farming management concept based on observing, measuring and responding to crop variability all to provide information to farmers in order to improve yields and use water smartly.

PF often uses various techniques in combination to achieve its goals:

- High precision positioning systems (like GPS) that drive farm technology navigation systems.

- Automated steering systems that enable farm mechanical systems

- Geomapping used to produce maps that detail soil type, with nutrient and pesticide levels

- Sensors and remote sensing that collect data from a distance to evaluating soil and crop health

- Integrated electronic communications between components in a system

Key questions for agricultural drone service providers

§§ 167 and 168: Depreciation is a Friend to Those in the Horse Business

Depreciation under §§ 167 and 168 is an important way in which horse businesses recover their costs. Horses are tangible assets and can be depreciated unless they are inventory, meaning if your business is buying and selling horses and not breeding or racing them then they are inventory and thus not depreciable.

Depreciating a tangible asset requires answering two questions:

- When can I take a depreciation deduction?

You generally start depreciating in the taxable year in which you engage in a trade or business, and your asset is “placed in service.” The placed-in-service date is the date the depreciable property is ready and available for a specific use, even if not actually used yet. Purchasing the asset is not enough, and if it was held for personal use and then converted to business use then the property becomes depreciable on the conversion date.

Generally, a racing or a show horse is placed in service the earlier of when their training begins, or when they start racing or are shown. And if previously placed in service, then they may be depreciated when purchased from the prior owner. For broodmares depreciation begins when the mare is first brought to the farm to be bred, and if already in foal then when purchased. A breeding stallion is placed in service when its services are first offered.

- How much can I take as a depreciation deduction?

Answering this question is a function of the following four elements:

The cost basis under §1012, and any adjustments under §1016. For example, a horse’s cost basis is increased by adding the cost of a trip to acquire it. Rul. 72-113, 1972-1 C.B. 99.

The depreciation method, as in the 150% declining balance Modified Accelerated Cost Recovery System (MACRS), for example.

The asset’s useful life, where horses generally fall into the three or seven year class, depending upon its age and use when placed into service. Yearlings, racehorses and breeding horses over 12 are depreciated as three-year property; all others are depreciated as seven-year property.

The depreciation convention, where generally the half-year convention is used unless the 40% rule is triggered under §168(d)(3) which requires the mid-quarter convention. The key is to determine in which quarter of the taxable year the asset is placed “in service.”

Note that selling depreciated property for a gain may result in recapturing some of the previously depreciated amounts as ordinary income.

§162: Deducting Equine Expenses

If your horse activity rises to the level of being a trade or business, and more than just a hobby (see §183), then congratulations! Subject to the passive loss limitation rules of §469, you are now entitled to recover some of those costs as §162 Trade or Business Expenses where expenses are generally deductible without limitation when they are paid or incurred:

- In carrying on any trade or business;

- Are ordinary and necessary, and,

- Are reasonable in amount.

“Ordinary” refers to those expenses that are common in your industry, and “necessary” does not mean absolutely necessary but instead means the expense is helpful to create income. The key here is that your business expenses should be similar to those in your industry and in line with similar budgets, where the amount expensed bears a reasonable relation to the benefit expected. It does not mean that you have to be a carbon copy of another business; however, you should be prepared to explain yourself to the tax authorities if asked.

Note that when taxpayers establish that they have incurred deductible business expenses but are unable to substantiate the exact amounts, the tax court can estimate the deductible amount in some circumstances, but only if the taxpayers present sufficient evidence to establish a rational basis for making the estimate. Cohan v. Commissioner, 39 F.2d 540 (2d Cir. 1930).

Cargo Drone Delivered to Alfred University Drone Club!

Today, Alfred University’s drone club (“Saxon Fly”) received a cargo drone – stay tuned for the next phase starting this fall.